Decrypting Authorization Flows: Tokenization Protocols That Secure Recurring Credit Card Charges Across Merchant Networks

Authorization flows for recurring credit card charges involve a sequence of steps where merchants initiate requests through payment processors and card networks, with tokenization serving as the core mechanism that substitutes actual card details with unique identifiers to reduce exposure during repeated transactions.

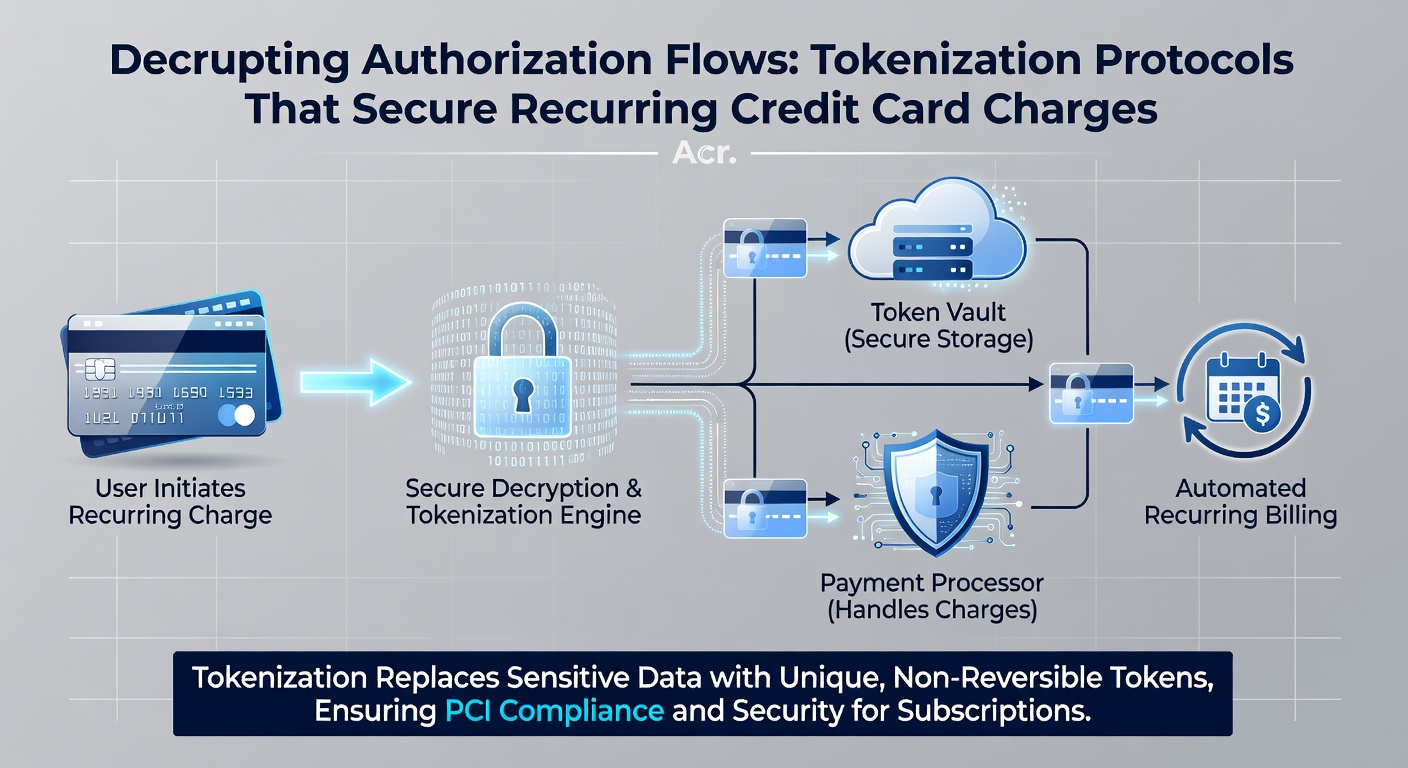

Authorization Flows in Recurring Payment Systems

Recurring payments begin when a cardholder grants initial consent during signup, after which merchants store a token instead of raw card data and submit authorization requests at scheduled intervals through gateways connected to acquiring banks and card networks. Each request travels from the merchant's system to the processor, which forwards tokenized information to the issuer for approval, and responses return along the same path to confirm or decline the charge while the actual primary account number remains shielded at every stage.

Data from the PCI Security Standards Council shows that tokenization aligns with requirements outlined in PCI DSS for protecting cardholder data in environments that handle repeated billing cycles, and organizations that adopt these methods report fewer incidents involving stored credentials because tokens hold no intrinsic value outside the specific merchant or network context.

Mechanics of Tokenization Protocols

Tokenization protocols generate unique tokens through cryptographic methods during the initial authorization, where the card network or a designated token service provider maps the real card number to a substitute value that merchants use for subsequent charges without ever receiving or retaining the original details. These tokens can be merchant-specific or network-wide, with the latter allowing limited interoperability across different processors when issuers approve the configuration, and the mapping database stays secured under strict access controls maintained by the token service provider.

Researchers at institutions such as those affiliated with the Bank for International Settlements have documented how these protocols integrate with existing payment rails to maintain compatibility while adding layers that prevent replay attacks or unauthorized reuse across unrelated merchant accounts.

Security Standards Governing Token Use

Standards established by global bodies require that tokens undergo validation during each authorization request, ensuring the token matches the expected merchant identifier and transaction type before the issuer releases funds, and this process incorporates dynamic elements such as cryptograms that change per transaction to further limit risk. In May 2026, updates to these frameworks continued to emphasize enhanced key rotation schedules and expanded support for network tokens that function across multiple regions without exposing underlying card data during cross-border recurring setups.

Observers note that compliance with these standards involves regular audits of token vaults and mapping systems, while merchants that integrate directly with approved providers gain access to real-time status checks that flag tokens requiring re-issuance due to card expiration or account changes.

Implementation Across Diverse Merchant Networks

Merchants operating subscription models connect their billing platforms to token service providers through APIs that handle the initial card capture and token generation in a single flow, after which recurring requests reference only the token and a stored payment agreement identifier. Large networks spanning multiple acquirers often employ network tokens that issuers provision once and allow authorized parties to use under defined rules, reducing the need for each merchant to maintain separate storage solutions while preserving the ability to update or revoke access centrally.

Case examples from organizations following guidelines issued by the Reserve Bank of Australia illustrate how token adoption in recurring billing environments supports high-volume operations without increasing the attack surface, since compromised tokens yield no usable card information to external parties attempting to replicate charges elsewhere.

Operational Benefits and Risk Mitigation

Tokenization reduces the scope of PCI DSS compliance for merchants because stored tokens fall outside the definition of cardholder data when properly segmented, which in turn lowers costs associated with securing full card details across distributed systems and simplifies incident response procedures when breaches occur. Issuers retain control over token lifecycle events such as suspension following suspected fraud, allowing them to interrupt recurring series without requiring the merchant to re-collect card information from the cardholder.

Figures released through industry reports indicate that networks using tokenized recurring flows experience measurable declines in unauthorized transaction attempts compared with legacy storage methods, and the architecture supports seamless handling of card updates through issuer-initiated token replacement programs that propagate changes without merchant intervention.

Conclusion

Tokenization protocols embedded in authorization flows provide a structured approach to securing recurring credit card charges by replacing sensitive data with non-sensitive equivalents that function reliably across merchant networks, and continued alignment with evolving standards ensures these methods address emerging requirements in payment processing environments. Organizations that implement these protocols maintain operational continuity while adhering to established security frameworks that govern data handling throughout the transaction lifecycle.